Principles

Principles

The curse of quarterly earnings has resurfaced with a post from Donald Trump, the President of the United States, on Truth Social strongly arguing for scrapping it.

In the grand theatre of Indian business, there is no ritual more sacred—or more misleading—than the quarterly earnings report. Every three months, it is a high-stakes corporate spectacle, a nationwide tamasha where armies of analysts parse every decimal point, and CEOs hold their breath explaining the deviation or departure of quarterly earnings.

The entire exercise is framed as a hallmark of a healthy, transparent market. Under SEBI's Listing Obligations and Disclosure Requirements (LODR), Indian companies are locked into this rigid system, required to submit quarterly financial results within 45 days of a quarter's end.

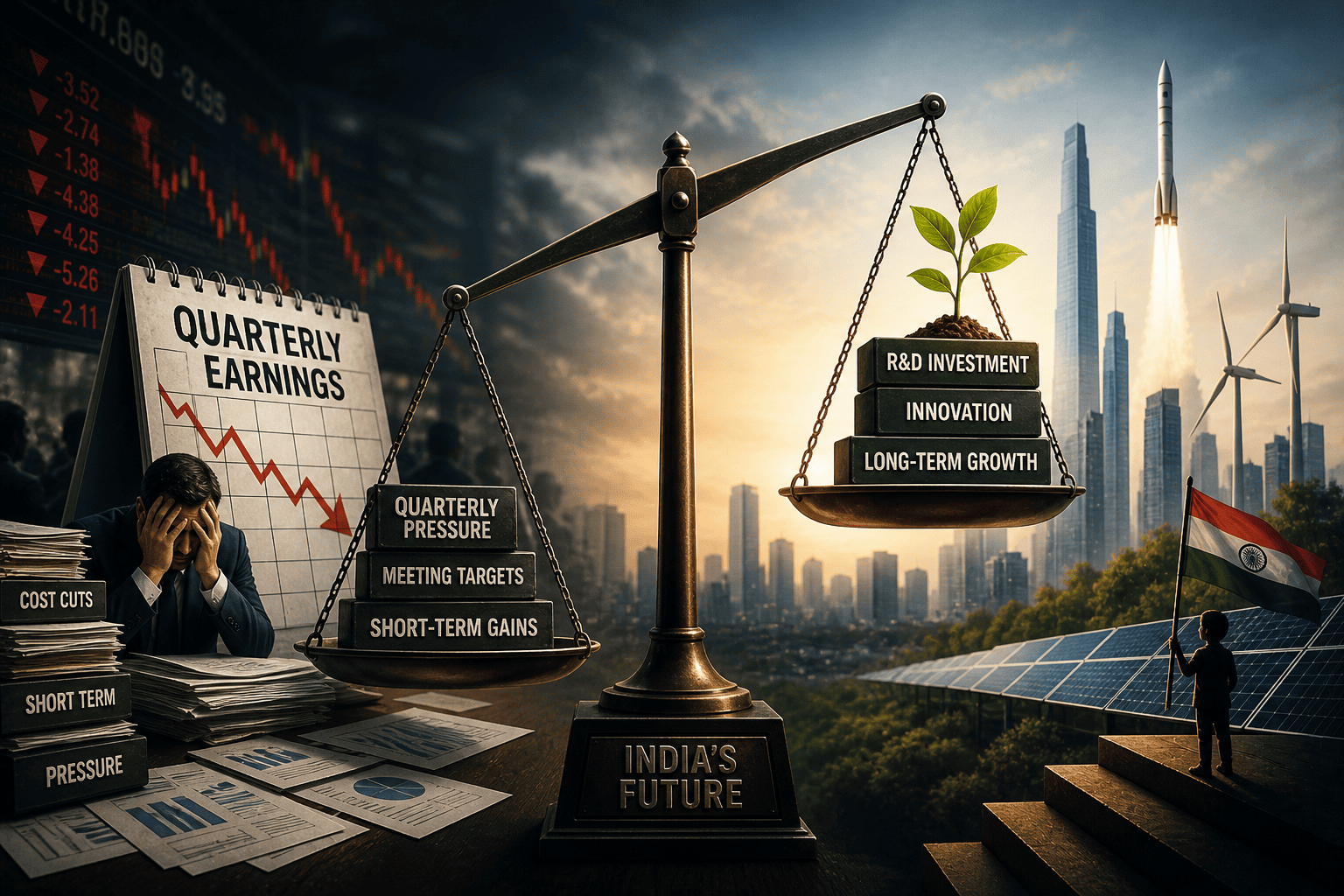

Yet, powerful voices, from legendary investor Warren Buffett, Jamie Dimon to former SEBI chairman M. Damodaran, have long argued that this ritual is not a sign of health but a slow-acting poison pill. They contend that the relentless pressure to meet short-term targets is forcing companies to sacrifice their long-term vitality.

Here is the central paradox of short-termism: the very pressure that strangles national innovation can actually be good for an individual company's bottom line.

In groundbreaking research by Stephen Terry of Boston University reveals the counter-intuitive finding that pressure to hit quarterly targets disciplines managers who might otherwise over-invest in R&D projects. This sharp-edged discipline can boost a firm's value —a tidy 1% gain in exchange for a little less daydreaming in the R&D labs.

But when every company adopts this short-sighted discipline, the cumulative effect creates a massive negative externality for the entire economy. When thousands of firms trim their R&D budgets to make the next quarter's numbers look good, they are collectively cutting off the nation's primary source of future growth.

It is a classic "tragedy of the commons" for innovation, where individually rational decisions lead to a collectively disastrous outcome.

Moreover, Global Research provides concrete evidence of the substantial costs imposed by quarterly reporting. According to SEC filings analysis, out-of-pocket cash expenses for quarterly reporting can reach $100,000 per reporting period for large companies, including fees to lawyers, auditors, tax experts, and IR/PR consultants.

The burden disproportionately affects smaller companies. Audit Analytics data shows smaller companies pay $3,345 per $1 million of revenue in audit fees, compared to just $541 per $1 million for large accelerated filers — a six-fold difference representing 0.33% versus 0.05% of revenue respectively.

Beyond monetary costs, management time represents a significant opportunity cost. Research indicates CEOs spend about 2% of their time and CFOs about 5% on quarterly filings.

Long before this global trend gained momentum, one of India's most respected regulators was already sounding the alarm. M. Damodaran, the former Chairman of SEBI, was a prescient voice calling for a fundamental rethink of this obsession with short-term metrics.

Speaking in a 2018 interview, he recalled his earlier, prescient warnings, noting wryly that the ideas being championed by Warren Buffett were ones he had advocated for years earlier. "This is not anything new, except the fact that it's coming from Warren Buffet, that is why everybody is sitting up and taking notice."

Indian CEOs like Uday Kotak, Kotak Mahindra Bank, Rohit Jawa, HUL, Vishal Sikka, Infosys, Chandrasekaran, when he was CEO of TCS, have passed a quip or voiced concern on undue pressure from quarterly earnings which compromises long term investment for the company and industry.

Conclusion: India at a Crossroads

The evidence is overwhelming. The quarterly reporting system, originally intended to promote transparency, is morphing into a value-destroying machine. It encourages a culture of short-term gamesmanship, forcing managers to sacrifice long-term innovation and national prosperity for the fleeting reward of meeting a quarterly number.

The European Union has already acted a decade ago. Japan has done the same in 2024, while Singapore has moved to a risk-based approach.

The result of this change was not chaos. When the UK removed the mandate, a crucial fact emerged: less than 10% of companies actually stopped issuing quarterly reports. An institutional imperative difficult to shrug in the garb of high standards of corporate governance.

The rise and success of China in the global innovation map, with limited data set for investors. The US companies have lagged, the staggering cost of inaction by them is immense.

Today, India's continued adherence to the old model is a conscious and increasingly risky choice. The current system primarily benefits short-term traders and analysts, not the long-term investors who are the true bedrock of a nation's capital markets.

The high churn by mutual funds is testimony to the short-term nature of the investment world. The rolling out of Production linked Incentives by the government are testimony of the fact that corporate R&D has been deprived for many years in the country.

Days are not far when quarterly earnings pressure will be called the innovation butcher. As the world is moving on in the hyper competitive mode, it is time for corporate India and regulators to find the courage to end the tyranny of the quarterly earnings syndrome.

***

Manish Bhandari, CIIA, founder of Vallum Capital Advisors, a Portfolio Management firm managing equity investments for Family Offices, NRIs and HNIs, serves as a Board Member of the Association of Portfolio Managers in India. Based in Mumbai, he can be reached at manish.bhandari@vallum.in.